Storm Damage & Insurance Claims in St. Clair, MO

St. Clair sits at the southern edge of Franklin County where Interstate 44 cuts the line between the St. Louis metro and the Ozark foothills, and that I-44 corridor is one of the busiest severe-weather tracks the National Weather Service watches every spring. When a supercell rolls up the interstate, the hail and straight-line wind hit the older steep-gabled roofs near the Highway 47 town center, the 1980s and 1990s subdivision ranches, and the rural acreage roofs out toward the Bourbeuse River bottoms all at once. After it passes, most St. Clair homeowners cannot see a thing from the driveway, and that is exactly when the claim gets won or lost.

We are not a St. Louis franchise that drives down I-44 only after the radar lights up. We have worked Franklin County storms since 1990 and put in-house family crews on roughly 2,400 Missouri homes, 306 of them in 2025 alone. When you call about hail on a roof off Springfield Road or wind-torn shingles on a place south toward the Meramec watershed, you reach the family whose name is on the truck. Tom Emmendorfer, founder Matt's son, gets on your actual St. Clair roof first, documents what the storm did, and is the one standing on it when your adjuster climbs up. That is the part no out-of-county landing page can fake.

What our storm damage & insurance claims includes in St. Clair

A storm claim is won or lost on documentation and on who is standing on the roof with the adjuster. Here is exactly how Tom runs it.

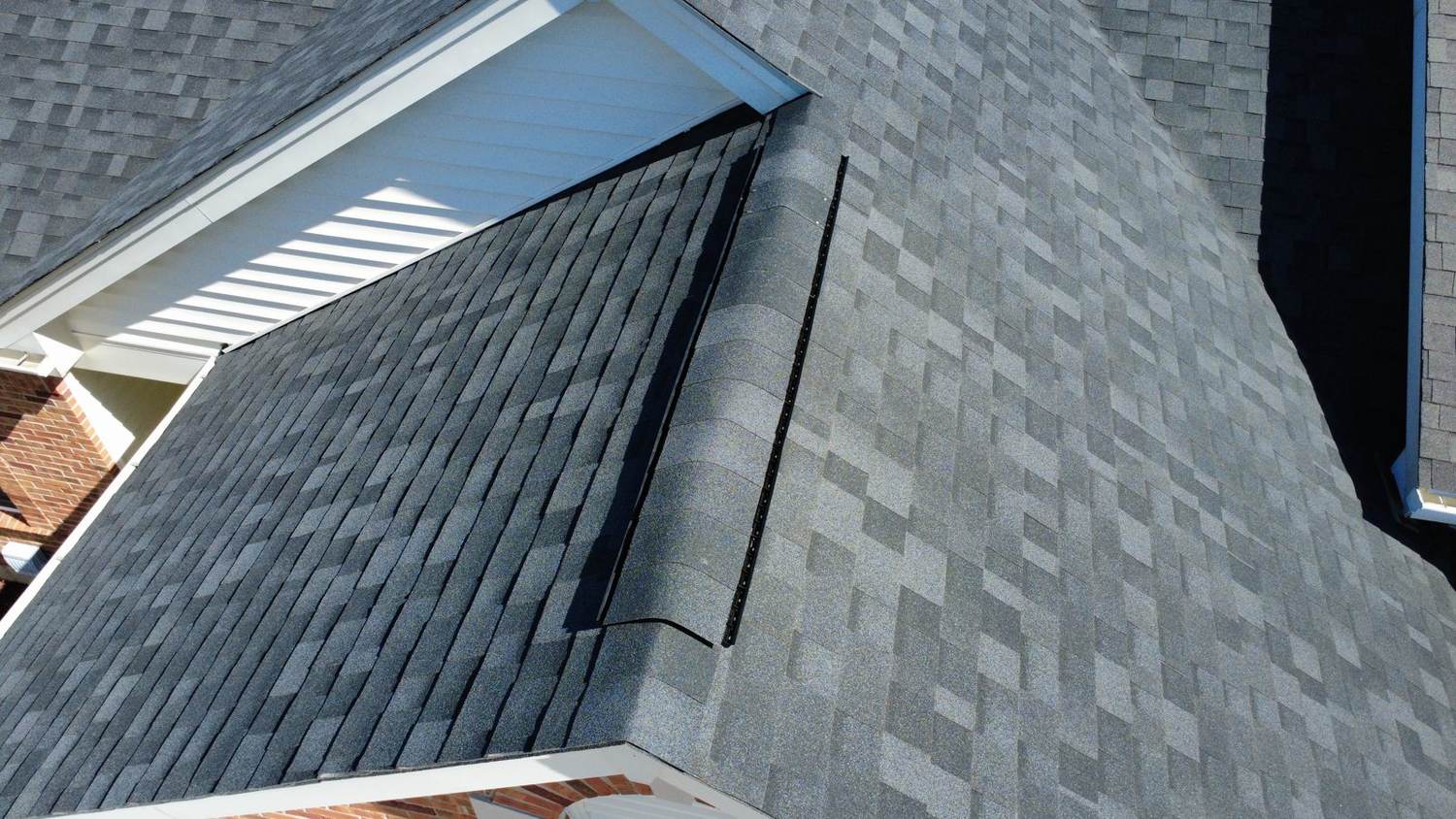

Free on-roof damage inspection

Call the roofer before the insurance company. Tom gets on your actual roof, not a satellite image, and documents hail bruising, wind-lifted shingles, granule loss, and damaged metal and flashing with photos. A written inspection from a real contractor creates independent evidence of the full damage scope before any adjuster forms their own opinion.

File the claim with your own carrier

If the damage is real, we help you open the claim with your insurer and pin it to the correct date of loss. Most Missouri policies require the claim within roughly one year of the storm, so a homeowner who notices a ceiling stain months after a spring hailstorm still has a window. We make sure the claim is filed clean.

Meet the adjuster on the roof

This is the step that wins claims. Tom is on the roof at the same time as the adjuster, walking every slope with him so the bruising and soft spots do not get written off. Under Missouri law you have the right to have your contractor present at the inspection, and we use it on every claim.

Supplement what gets missed or underpaid

Adjusters routinely miss damage or leave line items off the scope. We document what was skipped, send it back with photos, and go back and forth with the same or a different adjuster until the approved scope matches what the storm actually did. We do not have a problem doing it, and we make sure it gets done.

Replace or repair, then clean to no footprint

Once the claim is approved you pay your deductible and we handle the rest. Our in-house crews tear off, replace any failed decking and fascia we find, and install your CertainTeed, Owens Corning, Malarkey, or GAF system. Then we magnet-sweep for nails and haul every scrap so we leave no footprint behind.

St. Clair roofs rarely fail from one storm. It is the eastern Missouri stack. Spring and summer hail bruises the shingles and strips the granules, then a Missouri winter of freeze-thaw works that bruised material until the seams, flashing, and nail heads open up, and the next summer's hail finds the gaps. The federally declared March 2025 storms that moved through the county brought tornadoes, large hail, and straight-line winds over 75 mph, well past what it takes to start damaging asphalt. On a St. Clair claim that history matters, because the bruising from a storm two seasons back is still owed if it gets documented right, and Tom knows how to tie the damage to the correct date of loss before the adjuster forms his own view.

Storm Damage & Insurance Claims in St. Clair: questions

Get a free St. Clair storm damage roof inspection

Tom climbs your actual St. Clair roof, documents the hail and wind damage, and stands next to your adjuster so nothing gets missed. No subbed-out crews, no deductible games, same-day response just up I-44 in Union.

- We walk your actual roof before we quote it

- The manufacturer is named on your written estimate

- The price you approve is the price you pay

- Tom handles your insurance claim start to finish